Second charge market reaches 20-year high as 41,000 households unlock equity

09 March 2026

The UK second charge mortgage market has reached its strongest level in nearly two decades, with new figures highlighting how the sector is quietly becoming one of the largest specialist lending markets when measured by the number of borrowers it helps.

Figures from the Finance & Leasing Association (FLA) show that 41,657 second charge mortgages were completed in 2025, marking the highest annual total since before the financial crisis.

While the industry often focuses on the £2bn of annual lending, Loans Warehouse says the real significance of the latest figures lies in the number of customers now using the product.

The data equates to almost 4,000 completed loans every month, demonstrating the growing role second charge mortgages play in helping homeowners access capital without disturbing their existing mortgage.

Matt Tristram, co-founder of Loans Warehouse, said the specialist finance sector has historically compared markets by total lending value, but this can distort the true scale of lending activity.

“Most market commentary focuses on how many billions have been lent, but that doesn’t always reflect how many people are actually being helped,” he said.

“If we start measuring specialist finance markets by the number of borrowers helped rather than the billions lent, second charge lending is quietly becoming one of the largest sectors in the UK.”

Tristram said the difference becomes particularly clear when comparing second charges with other specialist finance markets such as bridging.

Data from the Bridging & Development Lenders Association (BDLA) shows the average bridging loan size is around £540,000, reflecting the sector’s focus on property investment and development finance.

By contrast, average second charge loans sit at around £50,000, meaning the two markets operate at very different scales in terms of loan size.

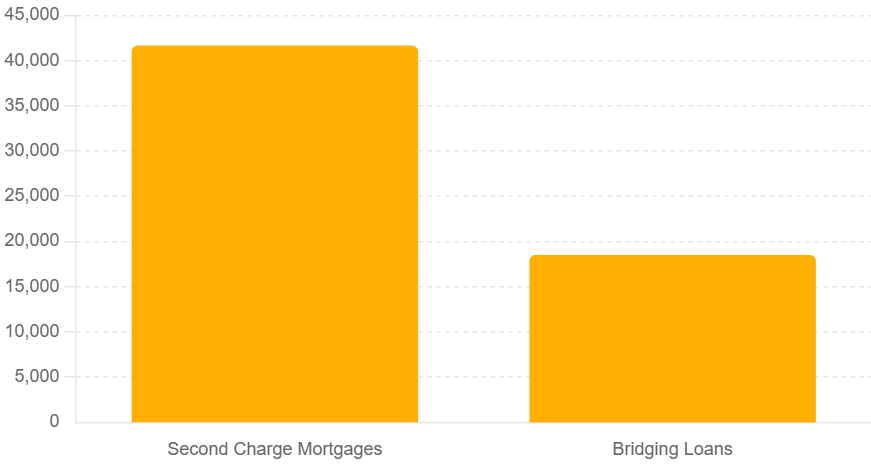

BDLA data suggests the bridging market completes around £10bn of lending annually across the UK. When combined with the average loan size of around £540,000, this implies the sector facilitates roughly 18,000–19,000 bridging loans per year, or around 1,500 transactions per month.

This compares with more than 41,000 second charge mortgages completed in 2025, equivalent to around 3,500 loans each month.

Estimated UK loan volumes (2025)

Estimated annual lending units show the second charge market now completes more than twice as many transactions as the UK bridging sector, despite significantly smaller average loan sizes.

Sources:

Finance & Leasing Association (second charge completions), Bridging & Development Lenders Association (average bridging loan size), estimated bridging transactions based on total lending divided by average loan size.

Loans Warehouse says this highlights why loan volumes can provide a clearer measure of market impact than total lending values alone.

“Bridging loans play a vital role in supporting property developers and investors, but they are typically much larger transactions, we love bridging, its a huge part of what Loans Warehouse offers” Tristram said.

“Second charge lending is fundamentally different. These are usually £40,000 to £60,000 loans used by homeowners to consolidate debt, fund home improvements or raise capital without refinancing their main mortgage.”

Tristram added that the growth in second charge completion volumes reflects how the market has evolved as borrowers look for ways to access equity while retaining historically low fixed-rate mortgages.

“For many homeowners, remortgaging simply doesn’t make sense when they are sitting on a low fixed rate,” he said.

“That’s where second charges have become a mainstream solution. When you step back and look at the numbers, the market is now helping around 4,000 homeowners every month, which shows just how important the sector has become in the wider lending landscape.”

Sources:

Finance & Leasing Association (second charge completions), Bridging & Development Lenders Association (average bridging loan size), estimated bridging transactions based on total lending divided by average loan size.